- Credit scores range from 300–850; higher scores mean better rates and more loan options.

- Mortgage lenders currently use older “Classic FICO” models (FICO 2, 4, and 5), but VantageScore 4.0 will soon be allowed as an alternative.

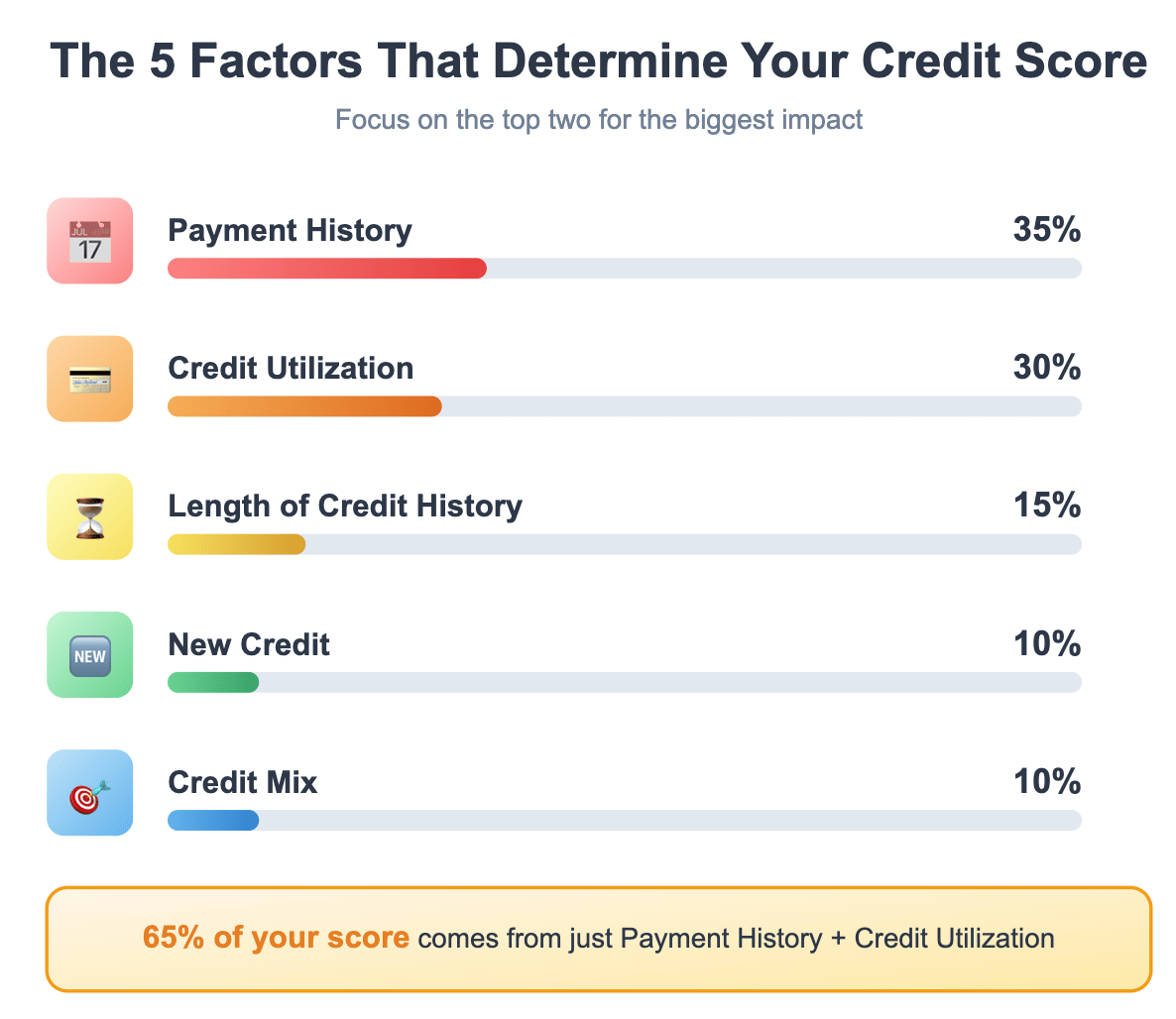

- Five key factors drive your score: payment history, credit utilization, length of history, new credit, and credit mix.

- Quick wins: pay down balances, fix report errors, keep old accounts open, and avoid new credit before applying for a mortgage.

- Even a 0.5–1% lower interest rate can save you hundreds per month and tens of thousands over the life of a loan.

What is a Credit Score?

A credit score is a number between 300 and 850 that gives lenders a quick snapshot of how risky it might be to lend you money. It’s a very big part of whether you can qualify for a mortgage and what your interest rate will be.

That number is built from data in your credit report, like how often you make payments on time, how much debt you’re carrying, and how long you’ve had credit. The higher the score, the better you look in the eyes of a lender.

Understanding the 300-850 Scale

Here’s how the typical credit score range breaks down:

-

300–579: Poor – You’ll likely have a tough time getting approved, and if you are, expect higher interest rates.

-

580–669: Fair – You can get approved, but your interest rate won't be the best

-

670–739: Good – Most lenders see you as a reliable borrower.

-

740–799: Very Good – You’ll qualify for better rates and more favorable terms.

-

800–850: Excellent – This is where you want to be for access to top-tier credit offers.

Why Lenders Care

For mortgage lenders, your credit score is one of the quickest ways to measure how risky it might be to loan you hundreds of thousands, or even millions, of dollars. A higher score signals that you’ve built a history of responsible borrowing and on-time payments, which makes you a safer bet.

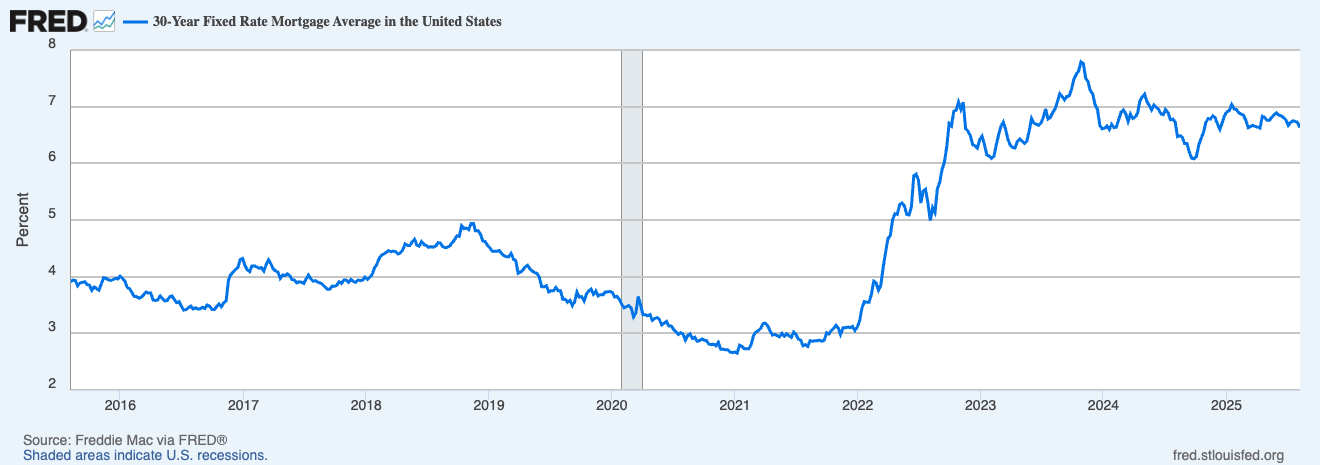

The reward for that strong track record? Lower interest rates, more loan program options, and often more flexibility during underwriting. Over the life of a mortgage, even a small difference in interest rates can add up to tens of thousands of dollars.

And because interest rates change over time, the timing of your purchase matters, too. Here’s how the 30-year fixed mortgage rate has moved in recent years, and why locking in a lower rate can make such a big difference:

FICO vs. VantageScore (and Why You Have So Many Scores)

If you’ve ever checked your credit score in one app and seen a different number somewhere else, you're not alone. It’s easy to be confused and wonder which one is real.

On any given day, you could have dozens of credit scores. That’s because your score can vary based on three main factors: the scoring model (like FICO or VantageScore), the version of that model (such as FICO Score 2 or FICO Score 8), and the credit bureau providing the data (Experian, Equifax, or TransUnion).

Each model has multiple versions. For example, VantageScore 3.0 and 4.0 are the most common versions used by consumer apps like Credit Karma and NerdWallet. FICO, on the other hand, has released more than 50 different versions over the years, each tailored to various types of lending, such as auto loans, credit cards, or mortgages.

The Scores That Matter for Mortgages

When it comes to buying a home, only a few of those many scores matter. Mortgage lenders typically rely on older “Classic FICO” models required by Fannie Mae for conforming loans:

-

FICO Score 2 (Experian)

-

FICO Score 4 (TransUnion)

-

FICO Score 5 (Equifax)

Lenders usually pull all three scores in a “tri-merge” report and use the middle score to make a decision. For joint applications, they use the lower of the two middle scores between the two borrowers, according to Fannie Mae’s representative credit score guidelines.

NEW in July 2025

In a massive development for homebuyers, the Federal Housing Finance Agency (FHFA) announced on July 8, 2025, that lenders will soon be permitted to use VantageScore 4.0 as an alternative to the traditional FICO scores when selling loans to Fannie Mae and Freddie Mac.

Why does this matter?

Because the current FICO models used for mortgages (FICO 2, 4, and 5) are based on algorithms that are 2-3 decades old. These older models don’t consider modern credit behavior and often exclude millions of borrowers with limited credit history. That includes many first-time buyers, younger adults, and people who pay rent and utilities on time but have few or no credit cards or loans.

VantageScore 4.0, by contrast, is designed to be more inclusive. It uses trended data and considers alternative payment histories, such as rent, utilities, and cellphone bills, to provide a more complete view of your financial habits. As highlighted in The New York Times, this could be a game-changer for borrowers with limited credit histories or scores that don't fully reflect their actual financial responsibility.

Many buyers already notice differences between their VantageScore and FICO numbers, sometimes 15 to 30 points or more. That gap could translate to better rates, better programs, and stronger offers, especially in competitive markets like Southern California.

While the industry is still waiting for full implementation, the direction is clear: credit scoring is evolving, and buyers who understand these changes early will have a strategic edge.

How Your Score Is Calculated

While FICO and VantageScore use different formulas, they both consider the same five key factors. However, the way they weigh these factors varies a lot, and that difference is essential, especially as VantageScore 4.0 becomes an option for mortgages.

IMPORTANT NOTE: Most lenders still rely on FICO scores when qualifying homebuyers. Therefore, it’s essential to understand how FICO works if you plan to buy a home soon. VantageScore may come into play down the road, but for now, here is what you need to know.

The Five Core Factors

These breakdowns apply to the versions mortgage lenders use today (FICO 2, 4, and 5):

-

Payment History: 35% (Most Important) Your record of paying on time is the most crucial factor. Recent late payments or collections have a much greater impact on your score than older ones.

-

Credit Utilization: 30% (Very Important) This is the percentage of available credit you’re using. Keeping your utilization below 30% is good, and below 10% is ideal for the best scores.

-

Length of Credit History: 15% (Moderately Important) Lenders prefer to see a long, stable credit history. Both the age of your oldest account and the average age of all your accounts matter. Closing old credit cards can reduce your score.

-

New Credit: 10% (Less Important). Each new credit application can lower your score. However, multiple mortgage or auto loan inquiries within 45 days are counted as one.

-

Credit Mix: 10% (Less Important) A healthy blend of credit types like credit cards, auto loans, and mortgages helps show you’re a responsible borrower.

Common Myths

Credit scores can be confusing, and there is often conflicting information about what harms them and what doesn’t. Before we discuss how to boost your credit score quickly, here are some common myths I hear—and what’s actually true.

Myth 1: Checking your credit hurts your score

Truth: Only hard inquiries hurt your score.

When you check your own credit through a monitoring app, a credit card company, or a lender doing a soft pull, it has no impact on your score at all. It’s only when a lender pulls your credit for a loan or credit application that it counts as a hard inquiry.

Myth 2: “I can’t check rates with a second lender because I don’t want another hard inquiry.”

Truth: Multiple mortgage inquiries within a short window are treated as one.

This is one of the most common misunderstandings I hear from buyers. Yes, applying for a mortgage triggers a hard inquiry, and yes, that can impact your score slightly, BUT credit scoring models are built to allow rate shopping.

So if you apply with multiple mortgage lenders within a defined time period (typically 14 to 45 days, depending on the scoring model), all of those inquiries are grouped together and count as a single event. This means you won’t be penalized for comparing lenders.

Myth 3: Carrying credit card debt helps your score

Truth: Carrying a balance doesn’t help, and it can actually hurt you.

The myth is that keeping a balance on your credit cards somehow builds your credit. It doesn’t. What matters is that you use your cards and pay them off on time. Carrying a balance increases your credit utilization, which makes up a significant portion of your score. It also costs you money in interest for no benefit.

Spoilers for our later sections, but if you want to build credit, try to pay down your balances ideally to under 10%, or at least under 30%, as soon as possible.

Myth 4: Closing credit cards will improve your credit score

Truth: Closing accounts usually does more harm than good.

Closing an older card, even if you no longer use it, can lower your score. That’s because it shortens your credit history and increases your overall utilization by reducing your available credit.

Even if you rarely use a card, keeping it open helps with both your credit age and your total available credit. If you want to simplify, consider putting a small recurring charge on it (like a subscription) and setting up autopay.

Myth 5: I can’t buy a house without good credit

Truth: You don’t need perfect credit to qualify for a mortgage.

Plenty of buyers become homeowners with credit scores in the 600s, or even the 500s, through certain loan programs. FHA loans, for example, allow scores as low as 580 with 3.5% down, and VA loans have flexible requirements depending on the lender.

Having excellent credit can help you qualify for better rates and lower payments, but it’s not a requirement to get in the door.

If your score needs work, here is a short guide to help you.

Quickly Raising Your Credit Score for a Southern California Home Purchase

Download → BOOST YOUR CREDIT SCORE: QUICK ACTION GUIDE

A better score will save you money. Even a slight boost in your credit score can mean a lower interest rate and a more affordable monthly payment. This could be the difference between buying your first home and renting. Perhaps buying a house instead of a condo.

Here is a real-life example: in Los Angeles County, the median sales price is $925,000 at the end of July 2025. With 20% down and today’s interest rate of 6.55%, your monthly principal and interest payment would be about $4,701. But if your credit score isn’t in the top tier and your rate rises to 7.55%, that same loan would cost you $5,199 per month, an extra $498 every month.

Now reverse it. If your monthly budget tops out at $4,000, a 6.55% rate gives you a purchase budget of roughly $786,956. But at 7.55%, your budget drops to around $711,600. That’s nearly $75,000 in lost buying power, just from a credit score difference. Note: these figures are principal and interest only and do not include taxes, insurance, or HOA costs.

Bottom line: improving your credit score can significantly improve your buying power and save you money. Below is a guide to quickly raising your credit score. (~30-90 days).

Step 1: Check Your Credit Reports and Fix Errors

Start by pulling your credit reports from all three bureaus (Experian, Equifax, TransUnion) and combing through them for mistakes. You can get free reports (via AnnualCreditReport.com), and you’re entitled to dispute any inaccuracies you find.

Common errors to look for:

-

Payments marked late that shouldn’t have been

-

Accounts that don’t belong to you

-

Old derogatory marks that should have aged off after 7 years.

If you find an error, submit a dispute right away – the credit bureau is required to investigate and correct inaccuracies.

Because you’re preparing for a mortgage, try to get any disputes resolved well before you apply. Mortgage underwriters may require that there are no open disputes during the loan process.

Step 2: Pay Down Credit Card Balances (Lower Your Utilization)

The fastest way to boost your credit score is to reduce your credit card balances. The portion of credit limits you’re using (your credit utilization ratio) is the second biggest factor in your score and the easiest one to manipulate. A good goal is to use under 30% of your credit limit, but for the best scores, aim even lower.

Should You Always Pay Down the Highest-Balance Card First?

Not necessarily. While it seems logical to attack the card with the biggest balance first, the credit scoring formula is more nuanced than that. FICO doesn’t just look at how much debt you’re carrying in total; it also looks at how that debt is spread across your cards and how close each card is to its limit.

Let’s say you have the following:

-

Card 1: $5,000 limit / $2,200 balance (44% utilization)

-

Card 2: $8,000 limit / $7,000 balance (88% utilization)

-

Card 3: $3,000 limit / $1,000 balance (33% utilization)

At first glance, you might think Card 2 is the clear priority because it’s nearly maxed out. And if you have enough cash to knock it down significantly, then yes, it probably makes sense to start there. High utilization on a single card, especially over 80–90%, can be a big drag on your score.

But if you don’t have enough cash to make a meaningful dent in Card 2, you will be better off paying down the smaller balances first.

Decision Tree

-

Do you have enough cash to knock Card 2 below a key threshold?

-

$3,000 gets it under 50% - worthwhile.

-

$5,600 gets it under 30% - a big score pop, and definitely worthwhile.

-

If you can cross one of those lines, Card 2 first is smart.

-

If you can’t cross a threshold on Card 2, but you can on the smaller cards…

-

Putting $700 on Card 1 (taking it below 30 %) and $1 000 on Card 3 (taking it to $0)

-

This lowers overall utilization almost as much as a $1,700 paydown to Card 2 – and drops the “high-balance-cards” count from three to one. Many people see a bigger immediate score bump this way.

-

After you’ve crossed breakpoints on the smaller cards, circle back to the maxed-out one.

Bottom line: If you can cross a key threshold on the high-balance card, go for it. But if not, it might be smarter to focus on smaller cards where your payments can push utilization below 30% or even pay them off entirely. Then, come back to the larger card when you can make a real dent in it.

Step 3: Make All Payments On Time & No New Credit Activity

This might be obvious, but if you are working your tail off to boost your credit, nothing will stop you in your tracks like missing a payment. Payment history is the #1 factor in your credit score calculation, accounting for about 35% of your FICO score. Even a single 30-day late payment can send your score plummeting (often by 90–100 points) and linger on your reports for 7 years.

Put every bill on autopay, and additionally set a reminder to check the account every month to ensure the autopay is still set up correctly.

If you have missed a payment recently and it was a one-time slip, contact the creditor to politely ask if they’ll refrain from reporting it (or remove the mark) as a goodwill gesture. There’s no guarantee they’ll agree, but it’s worth a try if you’ve otherwise been a good customer.

Avoid New Credit Inquiries or Accounts. This is true while building and while buying a home. There have been several occasions where deals have fallen through because a buyer purchased a new car while they were in the process of buying a home.

When you’re trying to raise your score in a short timeframe, hold off on any new credit activity that isn’t absolutely necessary. Each time you apply for a credit card, loan, or any financing, a “hard” inquiry hits your report and can temporarily ding your score a few points.

If you open a new account, it will lower the age of your credit accounts. Mortgage lenders in particular will scrutinize your credit habits in the months before closing. It’s best to avoid financing a new car, opening a store credit card, or any other credit moves until after you’ve secured your home loan.

Don’t close any old credit card accounts. Closing accounts can inadvertently hurt your score by reducing your overall available credit (which can raise your utilization ratio) and by shortening the average age of your accounts. Keep those long-held accounts open, even if you’re not using them heavily, because the length of credit history is another important score factor.

Bottom line: From here on out, keep your credit activity stable. Commit to a flawless payment record, don’t open or close any accounts.

Step 4: Become an Authorized User on a Strong Account (Optional)

Another way to boost your score, especially if your credit history is thin, is to be added as an authorized user (AU) on someone else’s well-managed credit card. When the account has a long history, a high limit, low utilization, and a spotless payment record, that positive history can appear on your credit reports, improving both your utilization ratio and the average age of your accounts.

When this can help:

-

You have a limited credit history and need to establish a track record.

-

You want to improve your utilization ratio by adding a high-limit, low-balance account.

-

You can benefit from a longer average account age to boost your score.

-

The account has 100% on-time payment history and low utilization.

Reasons it may not help (or could hurt):

-

The bank or card issuer does not report AU data to all three credit bureaus (Experian, Equifax, TransUnion).

-

The account has late payments or high balances. These will also appear on your report.

-

Your existing credit file is already well-established. If you have a long credit history, score gains may be minimal.

-

For mortgages, lenders may ask for proof you have a real relationship with the primary cardholder (per Fannie Mae’s Selling Guide).

How to check if the card reports AU accounts:

-

Call the card issuer’s customer service and ask if they report authorized user information to all three bureaus.

-

Search the card issuer’s help center or FAQ for AU reporting details.

-

Ask the primary cardholder to confirm their monthly statements show your name — this can indicate you’re set up in their system as a reported AU

Bottom line: Becoming an authorized user can be a fast way to strengthen your credit profile, but it works best when the account is in excellent standing and reports to all three credit bureaus. Choose the right account, confirm it’s reported, and avoid any that could bring negative history onto your report.

Summary: Small Changes, Big Impact

Raising your credit score might feel intimidating, but in many cases, meaningful progress is possible within 30 to 90 days. Reviewing your credit reports for errors, paying down balances strategically, making all payments on time, and avoiding new credit activity can all move the needle. Usually, this happens faster than people think.

In a market like Southern California, even a slight score improvement can lower your mortgage rate, boost your buying power, and save you tens of thousands over the life of your loan.

Whether you’re trying to qualify for your first home or stretch your budget from a condo to a house, improving your credit is one of the most powerful levers you have.

Start with what you can control, take it step by step, and if you’re not sure where to begin, I can connect you with a local lender who will review your credit and help you create a personalized game plan.

Feel free to call anytime with questions. (949) 230-6756